What is the Local Market Residual and how does it relate to the other factors in the Fabric Application?

In the article about factor models, we discussed the various types of factors present in the MSCI Multi-Asset Class (MAC) model. Within the Fabric application, the various risk metrics are computed using the Tier 4 Factors. These factors span multiple countries and many different asset classes.

The Tier 4 factors are themselves aggregated from local factors. The MSCI MAC model is constructed out of multiple tiers, from tiers 1 to 4, with the local factors forming a foundation for all subsequent tiers. Schematically, the MAC model has the following structure.

Multiple Tiers of the MAC Model

The schematic above shows the different tiers of the MAC model. At the lowest rung, forming the foundation, are the local factors. The local factors consist of a broad layer of detailed models, tailored to each market using local knowledge, deep data sets, and expertise in each asset class. These models include detailed factors – from Chinese Momentum to Japanese 10y rates to U.S. Early Stage Ventures and Offices in the City of London – to capture the drivers of each market.

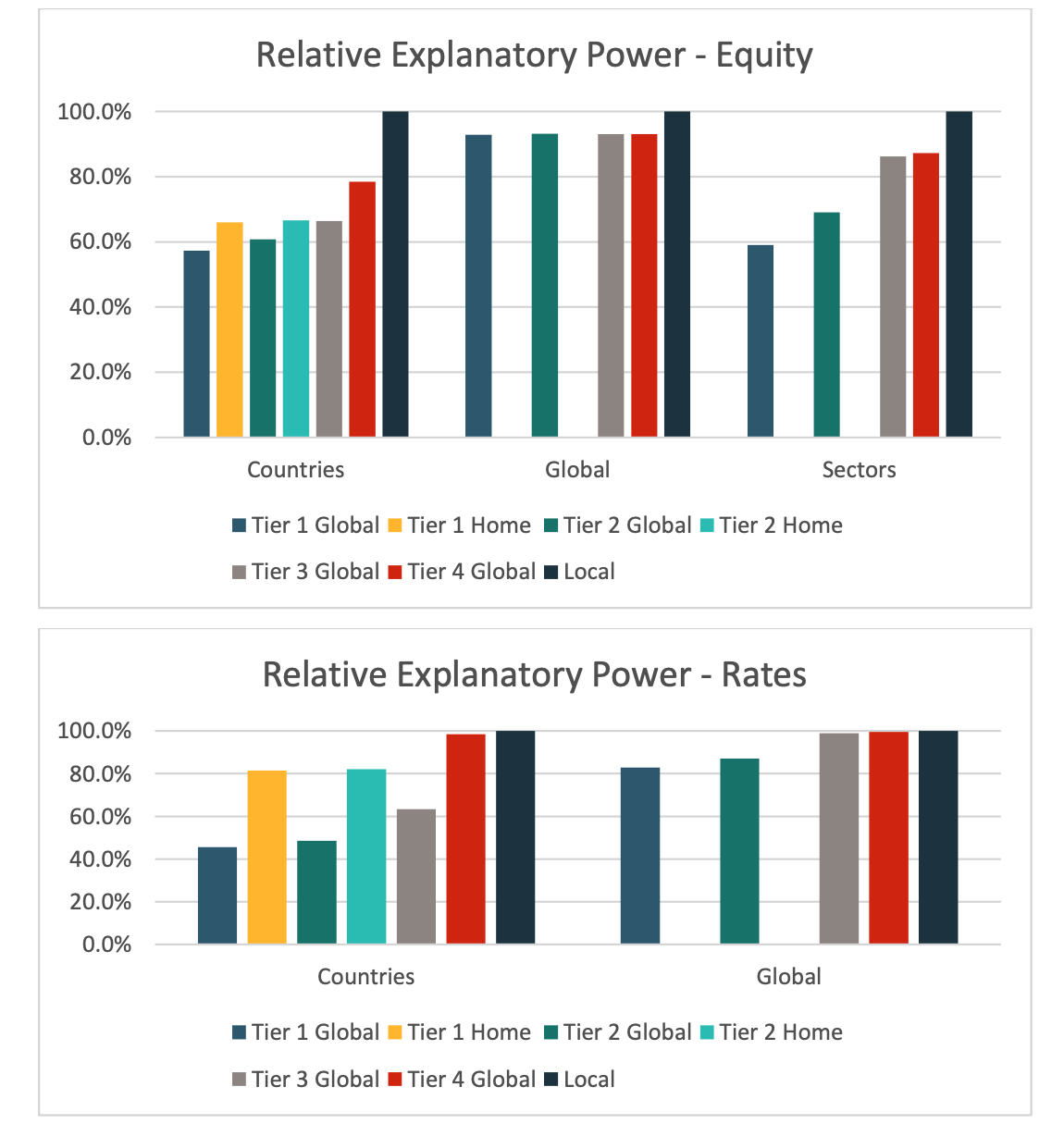

As we observe in the graphics above, Tier 4 factors are able to capture much of the explanatory power that the local factors have. Nonetheless, in the aggregation from the local factors up to the Tier 4 factors, loss of explanatory power is inevitable. While this might be reasonable from a modeling perspective, a loss of explanatory power also implies that there might be risks that are not being fully accounted for. Thus, we want to still have a complete picture of the risks in any given portfolio, and in turn account for the loss of this explanatory power upon aggregation.

Enter Local Market Residual

The local market residual term comes around to plug this gap. We recognize that for a given position or portfolio, its total risk should match when we use the local factor model or the Tier 4 factors. In formal terms:

where we have decomposed the total risk in two ways. First using the Local Factor, and then using the Tier 4 factors. Note that there will always be an inevitable Specific Risk term since there is always a fraction of asset returns that remain idiosyncratic.

Given that there is an inevitable loss of explanatory power, we expect to be missing a term --- marked as ?? --- in the equation above. This is the part of the total risk that is not accounted for within the Tier4 model and hence must be added explicitly so that the two computations match. The Local Market Residual is this "residual" term that must be present to have a complete picture of the total risk of any position or portfolio.

If we use the Tier 4 factors for risk attribution, then we need to add the Local Market Residual term to account for the loss of explanatory power. It is for this reason that the application includes this term in all the risk attribution charts.

Comments

0 comments

Please sign in to leave a comment.